Macro Pulse | July 1, 2026 | U.S. Macro Data Release

Growth Cools, Cost Pressures Ease. Warsh Won't Commit Yet.

Manufacturing missed. Payrolls missed. Construction missed. Hours earlier in Sintra, the new Fed Chair admitted inflation risk has come down but refused to draw a conclusion from it.

The Data

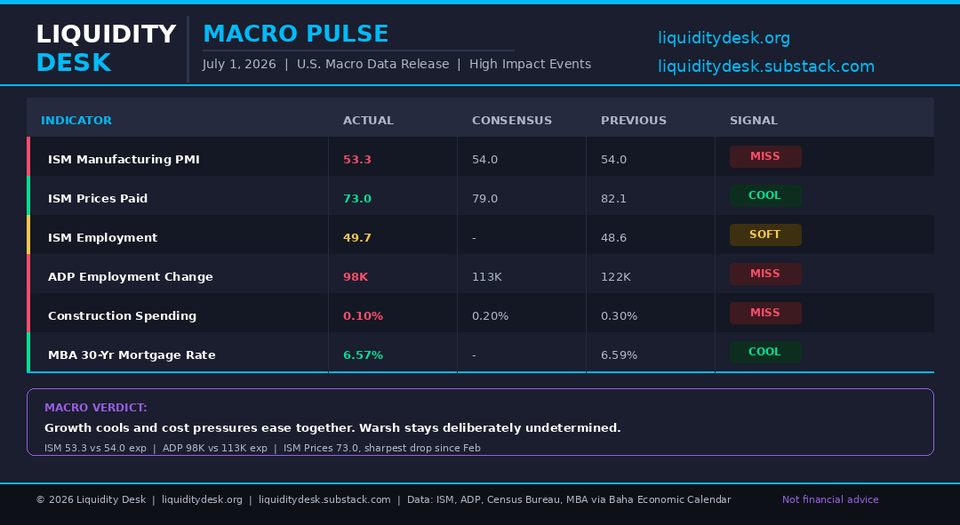

ISM Manufacturing PMI fell to 53.3 in June, down from 54.0 in May and below the 54 consensus. Output and new orders both grew at a slower pace than the prior month. The headline is soft, but two sub indices tell a more interesting story.

ISM Prices Paid dropped to 73.0 from 82.1, well below the 79 consensus. That is the sharpest one month decline since February, before the Middle East conflict disrupted oil supply and pushed input costs higher across the board.

ISM Employment rose to 49.7 from 48.6. Still contraction territory, but the softest pace of manufacturing job cuts in 15 months.

ADP Employment Change came in at 98,000 for June, below the 113,000 consensus and a clear step down from May's 122,000. Private hiring is decelerating.

Construction Spending rose just 0.1% in May, missing the 0.2% forecast and down from April's upwardly revised 0.3%. Residential spending gained 0.4% while nonresidential activity was flat, dragged by a 1.4% decline in manufacturing construction.

MBA 30-Year Mortgage Rate eased slightly to 6.57% from 6.59%, the lowest level in a month. Total mortgage applications held flat for the week.

The Standout Detail

The ISM Prices Paid drop is the number the market should not skip past. A move from 82.1 to 73.0 in one month, missing consensus by six full points, is the clearest signal yet that the energy driven cost shock from the Middle East conflict is starting to fade from the supply side. That is a genuine disinflation signal, and it arrived on the same day as a weak growth headline, which means it got buried under the ISM miss instead of leading the conversation.

What Does This Mean?

Speaking at the ECB Forum in Sintra hours before today's data, Fed Chair Kevin Warsh said that anyone who thought the central bank would be comfortable with an inflation objective above 2% would be disappointed. But he also acknowledged that inflation expectations and inflation risk have moderated recently, and explicitly said the Fed does not want to overdetermine things.

That is not a hawkish stonewall. It is a Chair who sees the same easing signal the market is seeing today and is choosing not to commit to a direction before he has to. Today's release gives him more reason for that caution, not less. Growth is slowing across ISM, ADP, and construction, but the labor market pain is easing rather than accelerating, and now the cost side is easing too. That combination looks more like an economy moving toward a soft landing than one sliding into a hard stagflationary shock.

Warsh also reaffirmed the Fed's independence following the Supreme Court's ruling on Fed Governor Lisa Cook, telling the Sintra audience the Fed is "calling balls and strikes" regardless of the political and legal backdrop. That is a signal to markets that institutional continuity holds at the Fed even as the legal fight around the Board continues.

What to Watch Next

The July jobs report and the next CPI print are the two releases that will either confirm or break today's signal. If both come in soft, the door to a rate cut later this year opens further. If either surprises hot, Warsh's wait and see posture becomes the market's justification for pricing out near term easing entirely.

Data: ISM, ADP, Census Bureau, MBA via Baha Economic Calendar Not financial advice.

Member discussion