Macro Pulse | Japan | June 18, 2026

Three Days After the Hike, Japan's Inflation Data Talks Back

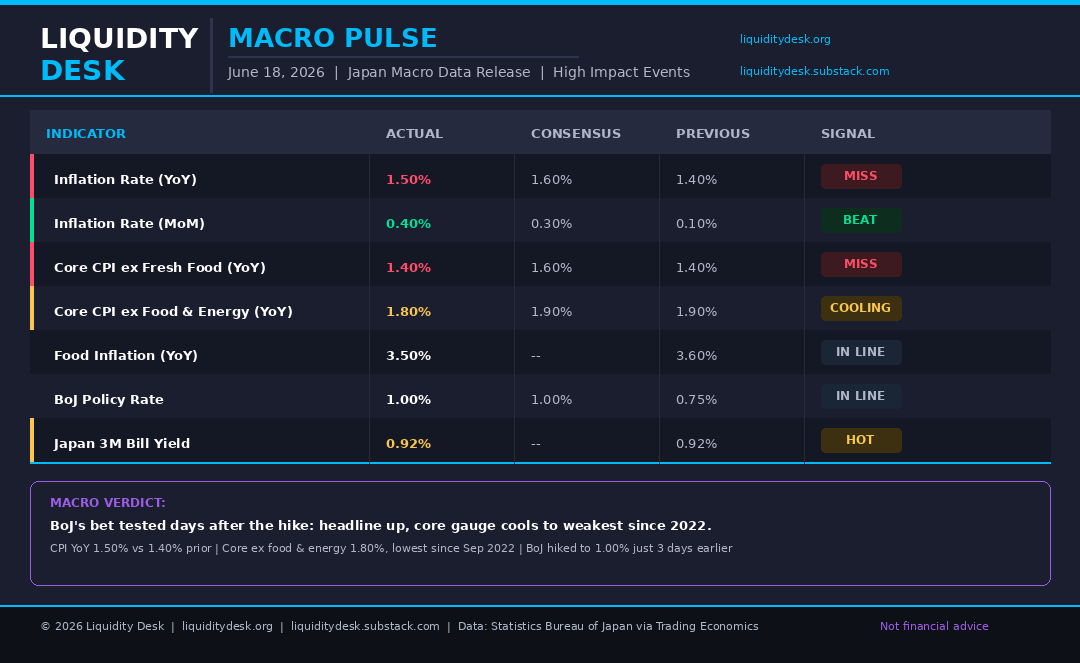

The Bank of Japan raised rates to 1.00% on June 16, the highest level since 1995, on a structural inflation call. Three days later, May CPI landed. The headline number supports the hawks. The number the BoJ actually watches does not.

The Split Read

Headline inflation accelerated to 1.5% year on year, up from 1.4% in April, though it missed the 1.6% forecast. Monthly momentum picked up too, with prices rising 0.4% against a prior reading of 0.1%. Food costs eased slightly to 3.5% from 3.6%, still the dominant driver of the consumer basket.

Core CPI excluding fresh food, the BoJ's primary policy gauge, held flat at 1.4%, missing the 1.6% forecast and still sitting well under target. The more telling number sits one layer deeper. Core inflation excluding both fresh food and energy, the cleanest read on demand-driven pricing, slowed to 1.8% from 1.9%. That is the softest pace since September 2022.

The Standout Detail

This is the gauge the BoJ leans on to separate energy noise from genuine domestic price pressure, and it just printed its weakest number in nearly four years, days after the bank justified a historic hike on the argument that underlying inflation could accelerate past target. The board hiked into a cooling core trend, not an accelerating one.

What Does This Mean?

The BoJ's case for June rested on preventing the Iran-driven energy shock from feeding into broader inflation expectations. This print does not validate that risk, at least not yet. Headline strength is being carried by energy and food pass-through, the exact channel the hike was designed to contain. The demand side of the economy, the part that determines whether 1.00% is the start of a real cycle or a one-off move, is softening.

The bond market has not blinked. The 3-month bill yield sits at 0.92%, just off its cycle high of 0.95%, pricing in the possibility of further tightening. That leaves a gap between what the rates market expects and what the inflation data is actually showing.

This fits the pattern building across the last several Japan editions. Machinery orders are tracing a declining trend beneath the surface. Services PMI stagnated earlier this year. The export surge that drove Q1 GDP was front-running, not organic demand. The BoJ hiked into an economy where the strongest signals are imported and the domestic signals are fading.

What to Watch Next

The July 31 BoJ meeting and quarterly outlook report will show whether the board treats this core softening as noise or as the first data point in a trend. Watch services inflation specifically. Tokyo CPI for June, released ahead of the national print, will be the next read on whether food and energy pass-through keeps masking a cooling core.

Source: Statistics Bureau of Japan, Bank of Japan via Trading Economics. Not financial advice.

Member discussion