Macro Pulse | Eurozone Flash CPI, June 2026 | July 1, 2026

The Hike That Missed Its Target

Three weeks ago the ECB raised rates and told markets inflation would stay well above target into 2027. The first flash data since that decision just proved the opposite. Eurozone inflation fell to 2.8% in June, down from 3.2% in May and below the 3.0% consensus. Core inflation dropped to 2.4%, also under expectations. This is not a rounding error. It is the sharpest one month deceleration since the Iran shock began.

The data

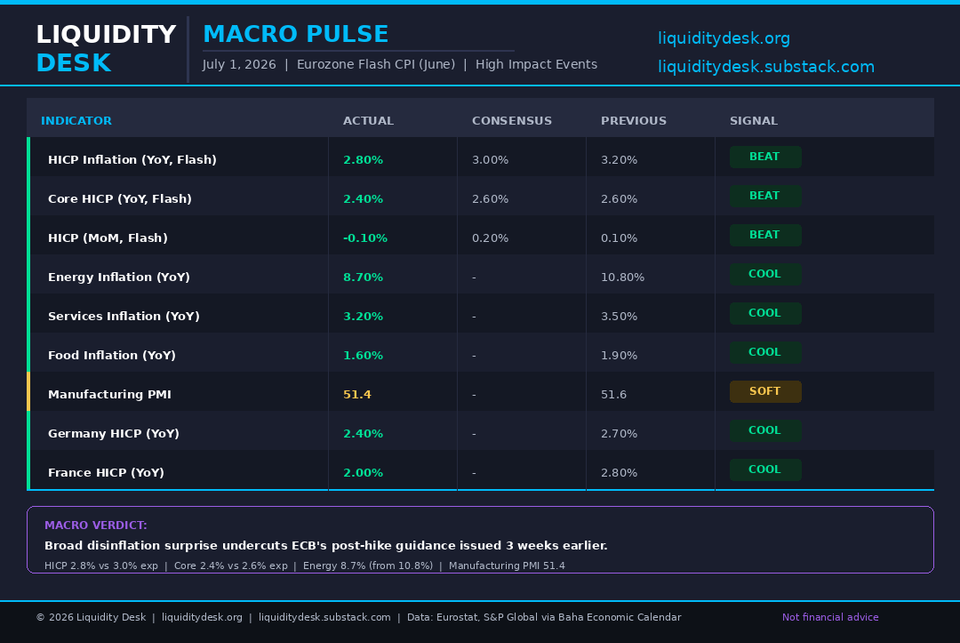

Headline HICP came in at 2.8% year over year, against a consensus of 3.0% and a prior reading of 3.2%. Core inflation, which strips out energy and food, fell to 2.4% from 2.6%, matching the low end of what the ECB itself had flagged as reassuring only weeks ago. On a monthly basis, prices fell 0.1%, the first monthly decline in five months.

The move was broad. Energy inflation cooled to 8.7% from 10.8%. Services inflation slowed to 3.2% from 3.5%. Food inflation eased to 1.6% from 1.9%. Germany's rate fell to 2.4% from 2.7%. France dropped to 2.0% from 2.8%. This is not a single component distorting the headline. Every major bucket moved the same direction.

Manufacturing PMI also softened, slipping to 51.4 from 51.6. Still in expansion, but the momentum that carried the sector through May is fading.

The standout detail

The market is treating this as a clean disinflation win. It may be missing the timing problem. The ECB hiked on June 11 explicitly because it judged the inflation path too risky to leave alone. Lagarde called the decision unanimous and described upside risks to inflation extending into H1 2027. Nineteen days later, the data moved directly against that call, and it moved on every axis the ECB was worried about, including services, which the ECB flagged as the sticky component least likely to fall quickly.

A single data point does not overturn a policy stance. But a hike justified by upside risk, followed almost immediately by a broad based downside surprise, is the kind of sequence that looks very different in hindsight than it did on the day of the decision.

What does this mean?

The ECB now has to explain a rate hike delivered against a backdrop of decelerating inflation across nearly every category it tracks. That does not force an immediate reversal. Central banks rarely change course after one data point, and Lagarde's guidance was explicitly meeting by meeting rather than precommitted. But it changes the balance of risks going into the July 23 meeting. The case for a second hike, which markets had started to price after June 11, gets harder to make if the July inflation print confirms this trend.

There is also a growth angle here. Manufacturing PMI easing at the same time inflation is falling faster than expected is not the combination a central bank wants to see right after it has tightened policy. If services PMI, due later this month, shows similar softening, the argument that this was a hike delivered at the wrong moment gets stronger. The 2011 parallel referenced in our last post remains the relevant risk case. It does not repeat automatically, but every data point that surprises to the downside on growth or inflation after a hike adds to that read.

What to watch next

July flash inflation data and the services PMI print will determine whether June was a one month deviation or the start of a trend. The ECB's July 23 meeting is now a genuine test of whether the June hike holds or gets walked back in tone if not in rate.

Data: Eurostat, S&P Global, Baha Economic Calendar.

Member discussion