Macro Pulse | China PMI Data | June 2026

China's June PMIs Just Beat. The Recovery Underneath Is Narrower Than It Looks.

China's headline PMIs cleared every hurdle in June. Manufacturing beat consensus. Non-manufacturing avoided the contraction economists expected. The composite hit a six-month high. On the surface, this reads like stabilization. Underneath, it's a story about which parts of the economy are actually growing, and it's a much shorter list than the headline suggests.

The data

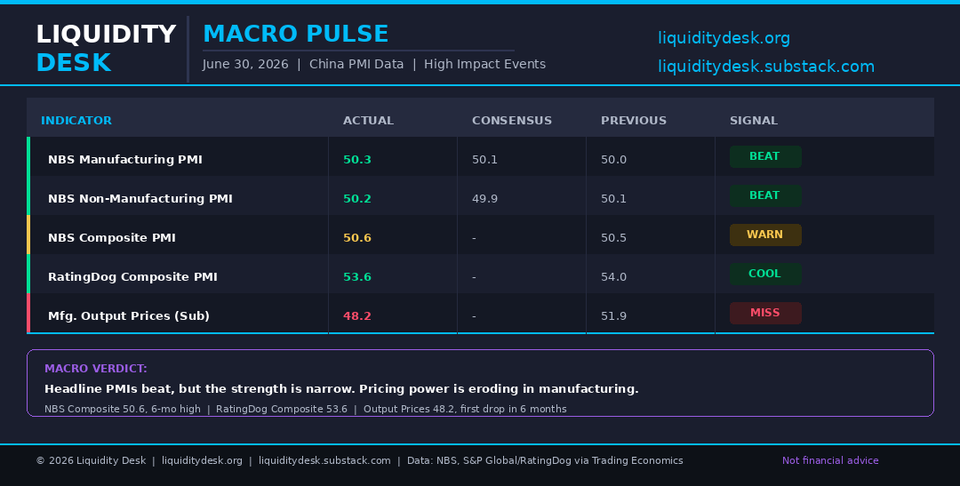

NBS Manufacturing PMI came in at 50.3, above the 50.1 consensus and up from 50.0 in May. It's the third straight month of expansion. New orders returned to growth after contracting in May, and foreign orders did too. Output accelerated. But employment stayed weak, extending a pattern this desk has flagged across multiple economies this year: production expanding without hiring.

NBS Non-Manufacturing PMI rose to 50.2, defying consensus expectations for a slip to 49.9. The strength here is concentrated. Telecom, IT and software services, financial services, and insurance all posted readings above 55. Air transport and real estate stayed below 50. Construction managed only 49, still technically in contraction despite an improvement from May.

The NBS Composite PMI reached 50.6, its highest level since December and the fourth consecutive month of expansion.

The private RatingDog Composite PMI told a similar but distinct story. It eased to 53.6 from a three-month high of 54.0 in May, but that's still among the strongest readings in three years. New business grew for a thirteenth straight month. Employment rose for a second consecutive month, the first back-to-back increase since mid-2023.

The detail the market is underpricing

Manufacturing output prices fell to 48.2 from 51.9, the first contraction in factory selling prices in six months. Input costs stayed elevated at 54.2. That gap is margin compression showing up directly inside the PMI survey itself, not just in the CPI-PPI spread this desk has tracked since June. Manufacturers are absorbing cost pressure instead of passing it through, which is a direct read on corporate profitability, not just on price levels.

What does this mean?

Markets are likely to read June's PMI beats as broad economic stabilization. The components don't support that read. Strength is concentrated in AI-linked exports and a narrow band of high-value services. Real estate and construction remain in contraction. Employment stayed soft in both official surveys even as output expanded.

There's also a supply-side wrinkle in the non-manufacturing beat. NBS's own commentary tied part of the services improvement to the central bank pressuring commercial banks to step up lending. That's an administrative lever, not organic demand recovery. It matters because it means the headline number is partly a policy input, not purely a market signal.

For the PBoC, this is a trap of its own making. Headline PMI strength gives policymakers room to hold off on fresh stimulus. But the internals confirm the decoupling this desk has tracked for months: the export and tech-driven segment of the economy is expanding while the domestic consumption engine stays stalled. Rates have sat unchanged for twelve straight months. Nothing in June's data changes that calculus.

What to watch next

Watch whether manufacturing output prices contract again in July. A second straight month would confirm margin compression is structural, not a one-off tied to a single survey period. Also watch the gap between the RatingDog and NBS composites. A widening spread says the private, export-facing economy is pulling further away from the officially measured one.

Data: NBS, S&P Global/RatingDog via Trading Economics

Member discussion