Macro Pulse | July 2, 2026 | U.S. June Jobs Report

The Jobs Report Confirmed the Warning. Nobody Is Hiring, and Fewer People Are Even Looking.

Yesterday's ADP miss was the preview. Today's payrolls report is the confirmation.

The Data

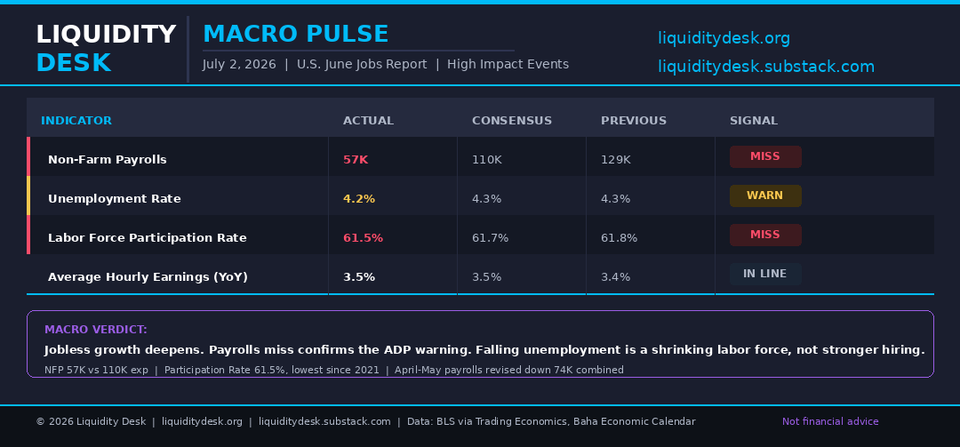

Non-Farm Payrolls rose by just 57,000 in June, well short of the 110,000 consensus and the lowest print in four months. It gets worse under the hood. April and May were revised down by a combined 74,000, taking May from an already soft 172,000 down to 129,000. This is now three straight months of downside surprises once the revisions land.

The sector breakdown shows where the weakness sits. Professional and business services added 36,000 and social assistance added 25,000, both solid. But leisure and hospitality shed 61,000 jobs, the sharpest one month drop in the report, likely amplified by World Cup related seasonal disruption on top of already soft demand. Retail trade lost 7,500. Financial activities, manufacturing, construction, and government all showed little to no change.

Unemployment Rate fell to 4.2% from 4.3%, technically a beat against the 4.3% consensus. Read the components before calling this good news. Total employment declined by 507,000. The labor force itself contracted by 720,000. The unemployment rate went down because people left the workforce faster than jobs disappeared, not because hiring picked up.

Labor Force Participation Rate dropped to 61.5%, the lowest level since March 2021, down from 61.8% in May and below the 61.7% forecast. The Employment Rate, the share of the population actually working, fell to 59.0%, a fresh four year low.

Average Hourly Earnings rose 3.5% year over year, in line with consensus and up slightly from 3.4% in May. Wage growth is holding, not accelerating and not breaking down. On its own this would read as a healthy signal. In this context it mostly confirms that the labor market's problem is not wage inflation. It is a shrinking base of workers.

The Standout Detail

The market will trade the unemployment rate. It should be trading the participation rate. A 4.2% unemployment figure sounds like improvement. It happened because 720,000 people left the labor force in a single month, the fastest contraction in the data this cycle. That is not the labor market healing. That is the labor market shedding its own denominator. Combined with two months of downward payroll revisions totaling 74,000, the June print does not stand on its own. It confirms a trend that started building in April.

What Does This Mean?

This is the release Fed Chair Warsh's Sintra remarks were waiting on. He told markets he did not want to overdetermine things before the data confirmed a direction. Today's data confirms one, and it leans toward the cooling side of his framework, not the hawkish side.

The signature here is not a hard landing. It is not stagflation in the classic sense either, since wage growth is not accelerating and Average Hourly Earnings came in exactly in line. What this looks like is the "low-hire, low-fire" pattern that first showed up in the JOLTS and ADP data back in April and May, now fully visible in the headline payrolls number. Employers are not laying off aggressively. They have also stopped hiring. And now, for the first time this cycle, workers are responding by leaving the labor force altogether rather than searching for jobs that are not being posted.

For the Fed, this removes urgency in both directions. It is not the kind of print that forces an emergency cut, but it is also not the kind of resilience that keeps a hike on the table. It hands Warsh exactly the ambiguous, wait and see data he said he wanted at Sintra, and it will likely keep him there through the next meeting.

Fed San Francisco President Mary Daly's comments today reinforced the same posture from the other direction. She said she sees no signs of a lack of resilience in the economy, pointing to strong AI driven capex and consumer spending holding up despite inflation. That view is not wrong on the investment side. It simply is not engaging with what today's participation and revision data are showing on the labor side.

What to Watch Next

The July CPI print is now the release that decides which of these two readings wins. If inflation confirms the cooling signal from the June ISM Prices Paid drop, the case for a cut later this year strengthens. If participation keeps falling and payrolls stay soft while CPI holds, the conversation shifts from "soft landing" to "labor force exit," a very different problem for policy to solve.

Data: BLS via Trading Economics, Baha Economic Calendar Not financial advice.

Member discussion